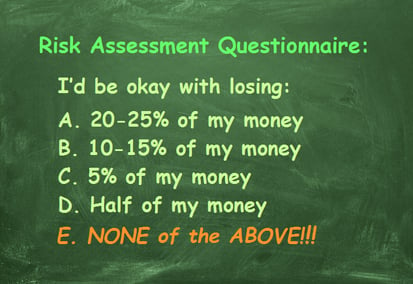

If you’ve ever met with a financial planner before, you were probably given a “risk assessment questionnaire” to complete before your meeting. This questionnaire is designed to assess how much risk you are comfortable with in regards to your investments.

If you’ve ever met with a financial planner before, you were probably given a “risk assessment questionnaire” to complete before your meeting. This questionnaire is designed to assess how much risk you are comfortable with in regards to your investments.

To create a risk assessment profile, you may answer questions like:

- Would you be willing to take risks in order to meet your long-term financial objectives

or would you rather protect your principal at the expense of future gains? - Would it be acceptable to experience a 30% loss if it was followed by a 30% gain later

on? (more on this later) - Will you need this money in ten, twenty or twenty-five years?

Your information would then be plugged into a computer program which would label you anything from conservative to aggressive, and would then generate recommendations of how to diversify your assets to achieve your goals.

Here are the problems inherent in this system:

1. The options presented are limited

If you’re presented with only a few choices of stocks or bonds, why would you question whether these are your only options? Representatives are often salespeople selling products from one large corporation, but be aware, even fee-based advisors are unaware of out of the box investment strategies (off of Wall Street).

2. Psychological pressure

Have you ever heard of the Milgram experiment? In short, subjects thought they were administering electric shocks to an unseen participant. Even when they thought they were causing harm, the subjects were unwilling to disobey authority and continued to give  shocks. While no electrical shocks are involved, many investors are unwilling to speak up or contradict a financial “expert” who surely knows best.

shocks. While no electrical shocks are involved, many investors are unwilling to speak up or contradict a financial “expert” who surely knows best.

The purpose of these questionnaire's is to convince investors that a certain level of risk is necessary. You might be told that you can afford to take some risk or that you even "need' to take a risk.

No matter what you're told, stock market risk is not a required rite of passage.

3. You are forced to act based on guesswork

These questionnaires force you to project how you feel about hypothetical financial scenarios that will determine your investments for decades to come!

4. The future performance of portfolios, no matter what you risk tolerance, is nothing more than a best guess.

Many advisors use the phrase "past results are no guarantee of future performance," when in reality the recommendations you are receiving are based on how similar investments performed in the past. One glaring problem with that approach is none of  the assigned categories, conservatively moderate, moderate, moderately aggressive and aggressive, present the possibility of a 45-50% loss, which many investors experienced in 2008-2009.

the assigned categories, conservatively moderate, moderate, moderately aggressive and aggressive, present the possibility of a 45-50% loss, which many investors experienced in 2008-2009.

Thus, investors are being asked to state how much they are comfortable losing, even though the advisor can't guarantee the portfolio will perform in those ranges.

- Safe investments do not provide decent returns.

- Only aggressive investors become big earners.

- It's okay to let someone else control your assets until you retire.

- It's not your advisor's job to protect your assets, only to help you assess your level of risk tolerance.

REDUCE YOUR RISK AND RAISE YOUR RESULTS!

Give us a call to learn how to take back control of your thinking and your money!

Sent from the Land of Possibilities!

Leave a comment